What makes Layer 1 blockchains the centerpiece of the current bull run, and can they prove their utility beyond speculation?

Layer 1s hit $2.8 trillion

Layer 1 blockchains have emerged as the focal point of the ongoing crypto bull run. According to data from CoinGecko, these foundational platforms have surged an astonishing 7,000% in value since January 2024.

This milestone comes on the heels of Donald Trump’s election victory, which appears to have reignited enthusiasm within the crypto space.

As of Nov. 29, L1 blockchains collectively command a market cap exceeding $2.8 trillion. Bitcoin (BTC), the dominant L1, accounts for nearly 70% of this market share. Trading at $98,300, BTC recently set a new all-time high of $99,600 on Nov. 22.

Ethereum (ETH), often hailed as the backbone of decentralized applications, has also seen significant gains. Up by over 34%, ETH is currently trading at $3,630.

Other L1 platforms are riding the bullish wave as well. Solana (SOL), a key competitor to Ethereum, reached an all-time high of $263.83 on Nov. 23 before pulling back slightly to $244, marking a 40% monthly gain.

Cardano (ADA) has taken the market by surprise with an impressive 200% surge over the past month, now trading at $1.09.

Emerging platforms like Hedera (HBAR) and Mantra (OM) have also shown exceptional performance, posting gains of 220% and 138%, respectively.

Mantra has been particularly remarkable, soaring over 6,000% since January. It peaked at $4.45 on Nov. 18 before retreating by 19.3%, currently trading at $3.54.

In contrast, Binance Coin (BNB), another major L1 platform, has lagged behind its peers. Despite trading at $658, it has delivered only a modest 10% gain over the past 30 days, making it a notable underperformer in this rally.

Are these gains a reflection of genuine growth in blockchain adoption and utility, or are they primarily speculative? Let’s dive deeper.

Ethereum’s TVL leadership

To gauge the performance of L1 blockchains beyond mere price action, it’s essential to consider their total value locked.

Essentially, total value locked (TVL) serves as a barometer of trust and activity within a blockchain ecosystem.

- High TVL typically signals robust adoption of DeFi applications such as lending, borrowing, and staking

- Low TVL may indicate diminished usage or waning interest.

Ethereum remains the unchallenged leader in this space, boasting over $70 billion in TVL as of Nov. 29 — an impressive 44% increase from $47.5 billion on Nov. 5.

A substantial portion of Ethereum’s growth stems from Lido (LDO), Ethereum’s premier liquid staking platform, which now accounts for nearly $35 billion of the network’s TVL.

Liquid staking allows users to stake their ETH while maintaining liquidity via derivative tokens, enabling further participation in DeFi activities.

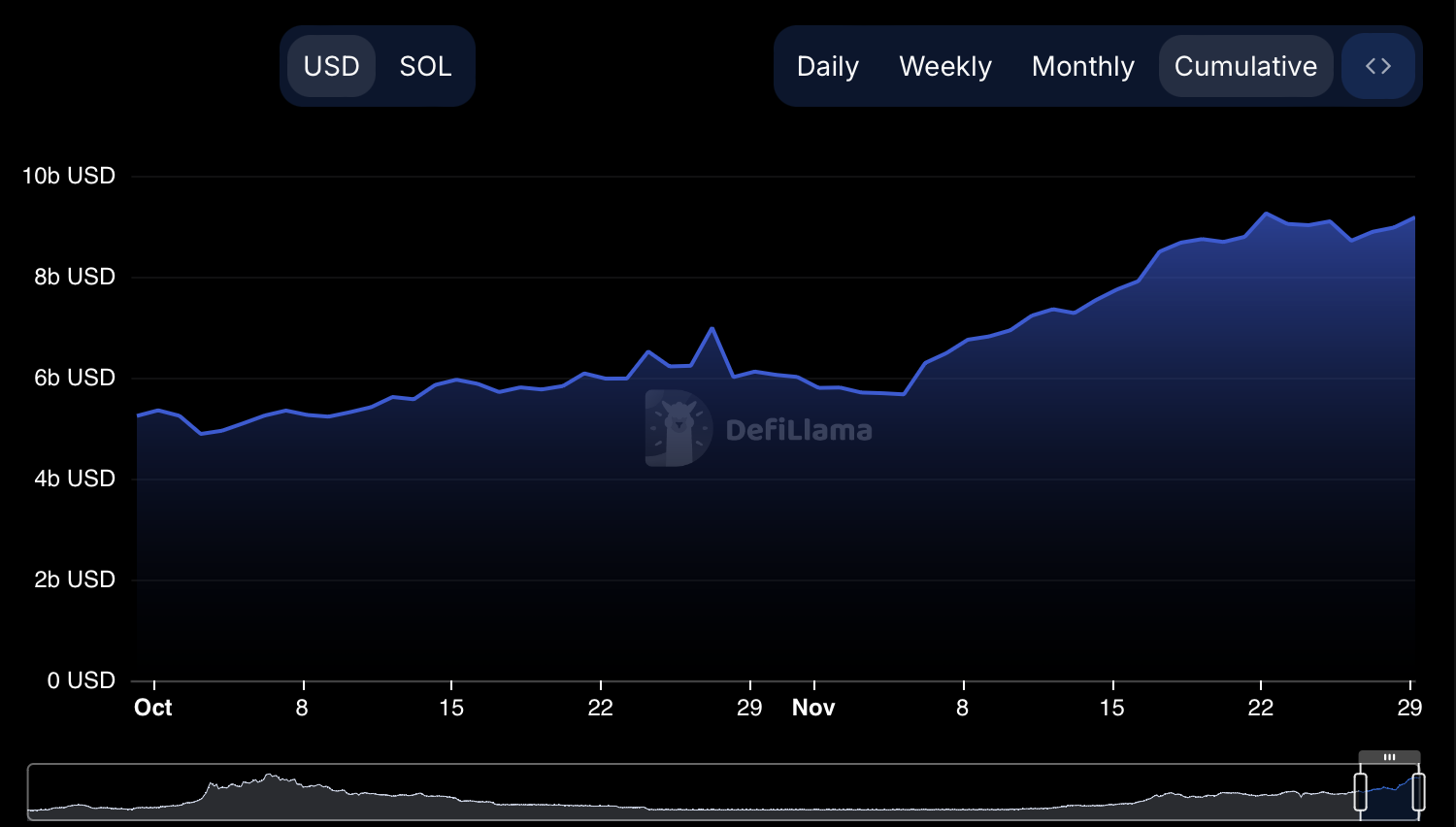

Solana has also shown notable progress, with its TVL climbing over 50% to $9.17 billion, bringing it tantalizingly close to its all-time high of $10 billion, last achieved in November 2021.

In contrast, Binance Smart Chain (BSC) has seen more modest growth. Its TVL increased by 17% over the past 30 days to $5.57 billion.

However, this figure is still significantly lower than its November 2021 peak of over $22 billion.

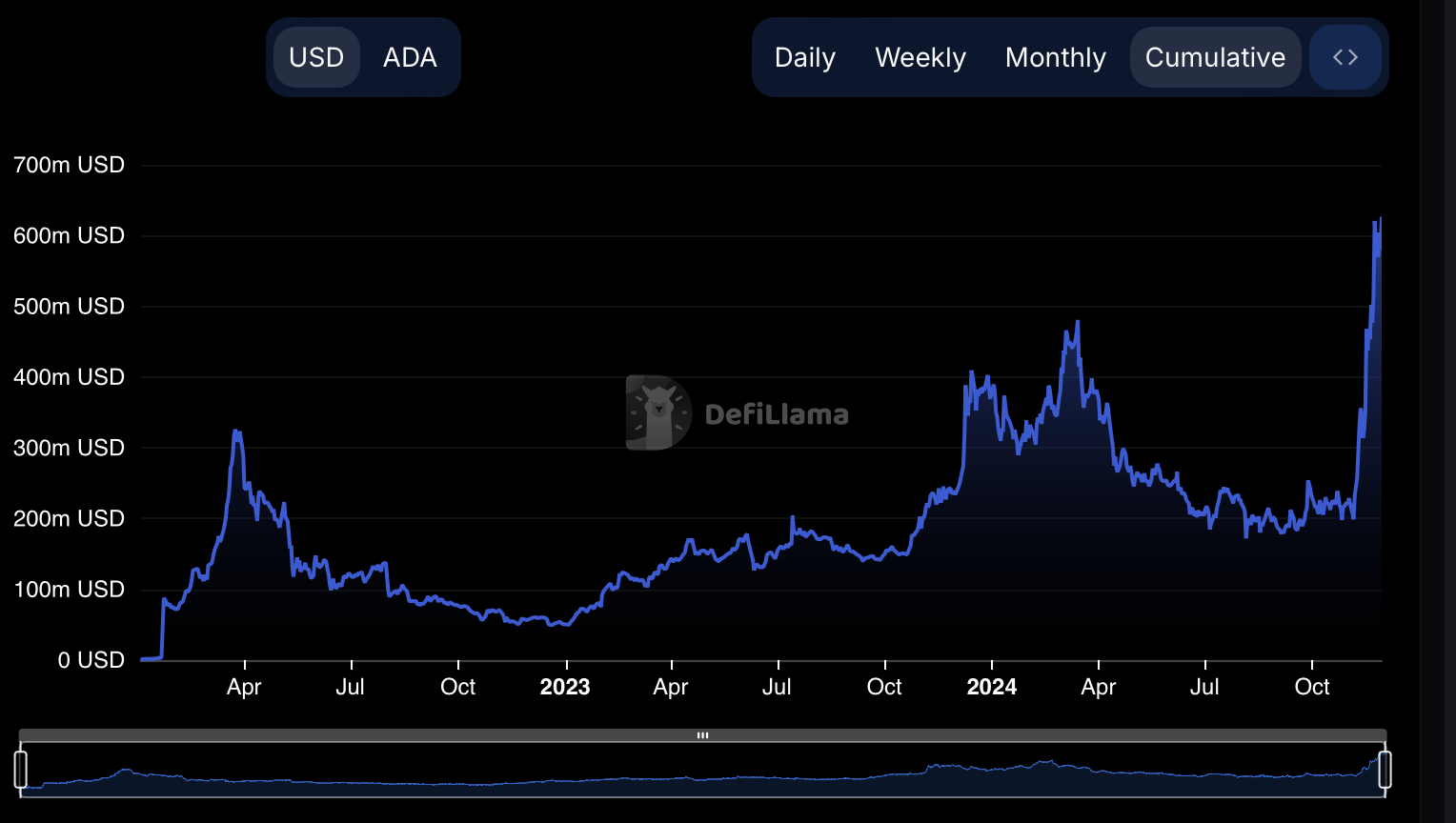

Meanwhile, Cardano has reached a milestone with its TVL hitting an all-time high of approximately $619 million. This marks a dramatic improvement from its sub-$1 million TVL levels in January 2022.

The fee race: Who’s winning?

Blockchain fees have long been a vital metric for assessing the activity, utility, and adoption of L1 platforms. They represent not only the cost users are willing to pay to transact but also the demand for block space and the overall health of the ecosystem.

During the bull run of 2020 and 2021, Ethereum dominated this space. Its fee revenue highlighted its position as the premier blockchain for dApps and DeFi.

In late 2020, Ethereum consistently generated over $1 million in daily fees, leaving competitors like Tron (TRX), which managed only a few thousand dollars a day, far behind. At that time, Binance Smart Chain and Solana had yet to emerge as key players in this metric.

By 2021, Ethereum’s fee revenue averaged between $20 million and $50 million daily during the second-half of the year.

Meanwhile, BSC generated $3 million to $10 million in daily fees, while Tron followed with a more modest $300,000 to $800,000. Solana, still in its infancy as a competitor, collected a relatively minor $100,000 to $200,000 daily in fees.

Fast forward to November 2024; Solana consistently outperformed Ethereum in daily fees throughout the month—a gigantic milestone reflecting its growing adoption and increasing network activity.

As of Nov. 28:

- Solana recorded $7.4 million in daily fees.

- Ethereum hovered around $6.19 million.

- Tron came in third with $2 million.

- BSC lagged behind at $680,000.

Ethereum’s relative decline in fee dominance is perhaps the most revealing shift. While it remains a powerhouse, several factors have contributed to its reduced share of the fee market.

The growing adoption of layer 2 and layer 3 scaling solutions has starkly lowered the fee burden on Ethereum’s mainnet. Additionally, waning interest from retail investors in recent months has further dampened activity.

What was once high fees justified by Ethereum’s unparalleled DeFi ecosystem are now being bypassed as users seek alternatives that offer comparable utility at a fraction of the cost.

The current state of the dApp ecosystem

The dApp ecosystem serves as the ultimate proving ground for L1 platforms, showcasing their ability to drive activity and engage users.

By analyzing transaction volumes and key contributors, we can uncover what fuels these networks and how they stack up. The data is as of Nov. 29.

Ethereum: Dominating volume, not value

Ethereum remains the heavyweight in DeFi, generating $175 billion in transaction volume across 4,844 dApps in the past month. Two standout platforms, Uniswap (UNI) V3 and 1inch, account for the majority of this activity.

Uniswap V3 alone processed $85 billion, solidifying its position as the cornerstone of liquidity provision and token swaps. Meanwhile, 1inch (1INCH) contributed $11 billion, attracting users with its efficient aggregation across multiple liquidity pools.

The data suggests that Ethereum continues to appeal to institutional and high-net-worth users who value its reliability and deep liquidity.

However, with only 1.76 million unique active wallets, it’s evident that high fees and scalability limitations are driving smaller users toward L2 solutions or alternative L1 platforms.

Ethereum remains the ecosystem for “big money,” but its retail appeal is diminishing as users seek more affordable options.

BNB Chain: The retail hub

BNB Chain has cemented its reputation as a retail-friendly ecosystem, processing $38.2 billion in volume from 5,555 dApps.

With 2.41 million unique active wallets—surpassing Ethereum—it’s clear that BNB Chain resonates with everyday users who prioritize low costs and ease of use.

PancakeSwap V2 is the standout performer, generating $11 billion in volume, nearly 29% of the chain’s total. BNB Chain also recorded 14.73 million transactions over the past month, highlighting its capacity for high-frequency, small-value interactions.

While these figures are impressive, the average transaction size is far smaller than Ethereum’s, reflecting BNB Chain’s role as a hub for casual traders rather than institutional players.

Moreover, regulatory scrutiny and government probes on Binance have also hindered its progress. To regain momentum, BNB Chain will need to attract more high-value projects.

Solana: Growing engagement

Solana dominates in raw activity, boasting 113.66 million unique active wallets and 594.7 million transactions over the past month.

These figures far surpass its competitors in sheer engagement. However, its $8.6 billion transaction volume indicates that the average transaction value remains modest.

The largest contributor to Solana’s volume is Pump.fun, a meme-driven platform responsible for $3.1 billion—about 36% of the chain’s total. Solana’s focus on high-frequency, low-cost interactions makes it a hub for speculative and experimental dApps.

Despite its impressive user engagement, Solana’s relatively low total transaction volume highlights its limited penetration into high-value DeFi markets. Even so, its rapid growth suggests it’s becoming the go-to platform for speculative, retail-friendly dApps.

Tron: The stablecoin workhorse

Tron processed $5.45 billion in volume from 63,660 unique active wallets and 953,220 transactions last month. While modest compared to Ethereum and BNB Chain, Tron’s strength lies in its specialization.

As the preferred blockchain for USDT transactions, Tron benefits directly from Tether’s massive daily trading volumes.

This focus on stablecoin transfers has ensured Tron’s relevance, but it also reveals a potential vulnerability. Without diversification into areas like gaming or broader DeFi applications, Tron risks being pigeonholed as the “stablecoin chain.”

Cardano: Slowly finding its feet

Cardano’s dApp ecosystem remains in its infancy but is beginning to show promise. With just 60 dApps, it generated $29 million in transaction volume from 40,250 unique active wallets in the past month.

While these numbers are modest compared to its peers, they reflect meaningful progress for a blockchain often criticized for its slow pace of development. Cardano’s focus on security and sustainability could attract developers and users over time.

However, it still has a long way to go before competing with platforms like Ethereum, BNB Chain, or Solana. Its future success hinges on expanding its dApp ecosystem and adapting to the evolving demands of the market.

The road ahead

The current bull market has thrust L1 blockchains into the limelight, highlighting both their strengths and their vulnerabilities.

Ethereum’s dominance in high-value transactions, Solana’s retail-driven activity, BNB Chain’s accessibility, Tron’s stablecoin specialization, and Cardano’s measured progress collectively illustrate a dynamic and evolving ecosystem.

However, the path forward will hinge on how these platforms tackle key challenges. Scalability remains a critical issue, as does the ability to attract and retain developers while steering off intensifying competition.

As prices continue to climb and adoption broadens, the true test for L1s will be sustaining this momentum. Proving their utility beyond speculative cycles will be crucial in cementing their place in the crypto space.

Whether this bull run signals the dawn of a transformative era or simply another chapter in crypto’s unpredictable journey depends on how these platforms adapt to meet the demands of an ever-growing global audience. The stage is set, but the story remains unwritten.